Blockchain is a key technology behind cryptocurrencies, but its reach goes far beyond that world. Its value lies in enabling multiple parties to share and verify information with a clear history.

What’s more, by relying on decentralization, it helps reduce single points of control and coordinate participants under common rules. But that’s not the only thing you should know about this system.

Stick around to discover what blockchain is, how it works, the types that exist, and the cases where it’s used.

Blockchain: What It Is, How It Works, Types, and Examples

What Is Blockchain?

Blockchain is a technology that stores transactions securely and immutably in a distributed database without intermediaries. This means multiple participants can verify the information and keep it synchronized.

The key is that information is grouped into blocks linked to each other, forming an ordered chain of records. If someone tries to modify a block, the change is detected because it breaks the continuity of the chain, which ensures the integrity of the recorded data.

Also, because it doesn’t depend on a single entity, it’s useful in systems that seek trust, transparency, decentralization, and shared control.

How Does Blockchain Technology Work?

The blockchain operates through a structured process that allows information to be created, verified, and stored reliably.

Here’s the sequence it follows:

Creation of a transaction or record: for example, a payment, data exchange, or any information you want to add to the history.

Validation by the network (nodes): that transaction is sent to the network for review and confirmation that it meets the system’s rules.

Grouping into blocks: validated transactions are grouped together to be incorporated into the records and keep chronological order.

Cryptographic linking: each block is connected to the previous one, creating a continuous chain. This link protects the history because any attempt to modify a block would affect the ones that follow.

Distribution of the ledger across multiple nodes: finally, the record is updated and kept in sync among the network’s participants so everyone works with the same information.

Tip: if you want to visualize a transaction’s journey, flowcharts are ideal for showing the steps from creation to confirmation and addition to the chain.

Key Components of Blockchain

This model stands on several basic components that work together:

Blocks: the units where information is grouped.

Nodes: the network participants who maintain copies of the ledger and help verify information.

Distributed ledger (DLT): the shared record replicated across nodes.

Cryptography: used to protect information and ensure records can’t be altered without the change being detectable.

Consensus mechanisms: the rules the network uses to agree on what information is valid before adding it to the ledger.

Types of Blockchain

Blockchain technology is classified into different types depending on who can participate in the network and how data validation is managed.

Accordingly, we have:

Public blockchain. An open network where anyone can join, view the history, and participate in network operations according to its rules. Common in projects aiming to be global, for example, Bitcoin and Ethereum.

Private blockchain. Operated by an organization or designated administrator, so access and validation are restricted.

Hybrid or consortium blockchain. Combines elements of public and private blockchain. Useful when multiple parties want to collaborate without opening the entire ledger to the public.

In general, a public blockchain favors openness and transparency, which is why it’s often used for open systems.

Private and consortium blockchains, on the other hand, are common in inter-company processes, traceability, and shared networks among organizations.

What Is Blockchain Used For?

Blockchain is used to record and validate information in a shared way with a verifiable history. In some cases, it’s combined with AI tools to analyze patterns, detect anomalies, and automate reviews over large volumes of records.

And its applications go far beyond cryptocurrencies.

In essence, it’s used for:

Finance and payments. Recording money transfers and movements with greater traceability.

Cryptocurrencies. Keeping the record of transactions and ownership of digital assets.

Supply chain traceability. Recording a product’s journey and lifecycle, making it easier to verify origin, stages, and movements.

Smart contracts. Automating agreements that execute when certain conditions are met, reducing friction and time in repetitive processes.

Data and records management. Certifying documents and critical histories (for example, in digital health), with verifiable evidence of changes.

Electronic voting. Being explored for systems where auditing the process and maintaining a verifiable record are key—though it depends on system design.

Digital identity. Verifying credentials and sharing data in a controlled way, reducing duplicate validations and improving access management.

The blockchain system adapts to processes where transparency, traceability, and record integrity matter. Below are some examples…

Real-World Examples of Blockchain Use

Today, blockchain technology is used or being implemented in different contexts to solve common problems:

Product tracking (logistics): companies like Walmart have used blockchain to trace the origin and journey of certain products.

Smart contracts and public procurement: the Blockchain HACKMX initiative proposed a pilot to digitize tenders, seeking greater traceability and transparency in the process.

NFTs and digital assets: platforms like OpenSea operate with NFTs, whose ownership and transfers are recorded on blockchain.

Identity verification: projects like EBSI (European Union) promote the use of verifiable credentials and DIDs (Decentralized Identifiers) to share and validate specific data with more user control and verification without intermediaries.

It’s worth noting that every implementation varies depending on the type of network, access level, operating cost, and the problem being solved. That’s why blockchain is often understood as infrastructure that brings traceability and verification when the context justifies it.

Advantages and Disadvantages of Blockchain

Before using blockchain or adopting it in a project, it’s worth reviewing the pros and cons:

Advantages of Blockchain

Operates transparently, allowing the history of records to be consulted and verified jointly.

Keeps data immutable—once recorded, they’re very difficult to modify without leaving a trace.

Offers greater security by reducing manipulation risks and avoiding reliance on a single point of control.

Reduces the presence of intermediaries, simplifying validation of transactions and records in certain processes.

Trust is anchored in shared rules and the network, not a single entity.

This approach also relates to models like RFM, since blockchain strengthens the quality, traceability, and reliability of analyzed data.

Disadvantages of Blockchain

Some networks can become slower or more expensive as the volume of transactions or participants grows.

Depending on the validation mechanism, certain blockchains may require high energy consumption.

Implementing and maintaining blockchain solutions may require specialized knowledge and a well-thought-out architecture.

In many countries and sectors, the rules around blockchain’s uses, responsibilities, and compliance are still evolving, which can create uncertainty.

These limitations don’t invalidate the technology, but they do show that adoption should be evaluated based on context and use case.

Blockchain Beyond Cryptocurrencies

Although many people immediately associate it with Bitcoin, blockchain is not the same as cryptocurrencies. In reality, Bitcoin is just one of the best-known applications of this technology.

As noted, the blockchain is useful in other contexts. In the corporate environment, for example, blockchain has been explored as a tool to improve multi-party processes—especially when there are documents, validations, and information transfers that typically rely on intermediaries.

That’s why it’s attracted attention in sectors like logistics, finance, identity, and records management. Why? Because its priority is to maintain a verifiable and shared history.

Seen this way, it functions more like a technological infrastructure on which solutions are built—whether to record data, coordinate actors, or reduce friction in specific operations.

Therefore, it can also add value in distributed environments—especially when integrated with remote-work tools to coordinate access, audits, approvals, or document traceability among teams in different countries.

Conclusion

Blockchain has established itself as a foundational technology for building digital trust when multiple actors are involved. By functioning as a distributed ledger, it enables participants to share information with greater transparency, control, and consistency. This reduces friction in processes that depend on constant validations and a verifiable history.

However, blockchain isn’t always necessary; its value depends on the system’s context and goal. But when evidence, auditability, and coordination among parties are required, it provides a solid base for recording, verifying, and operating with greater certainty.

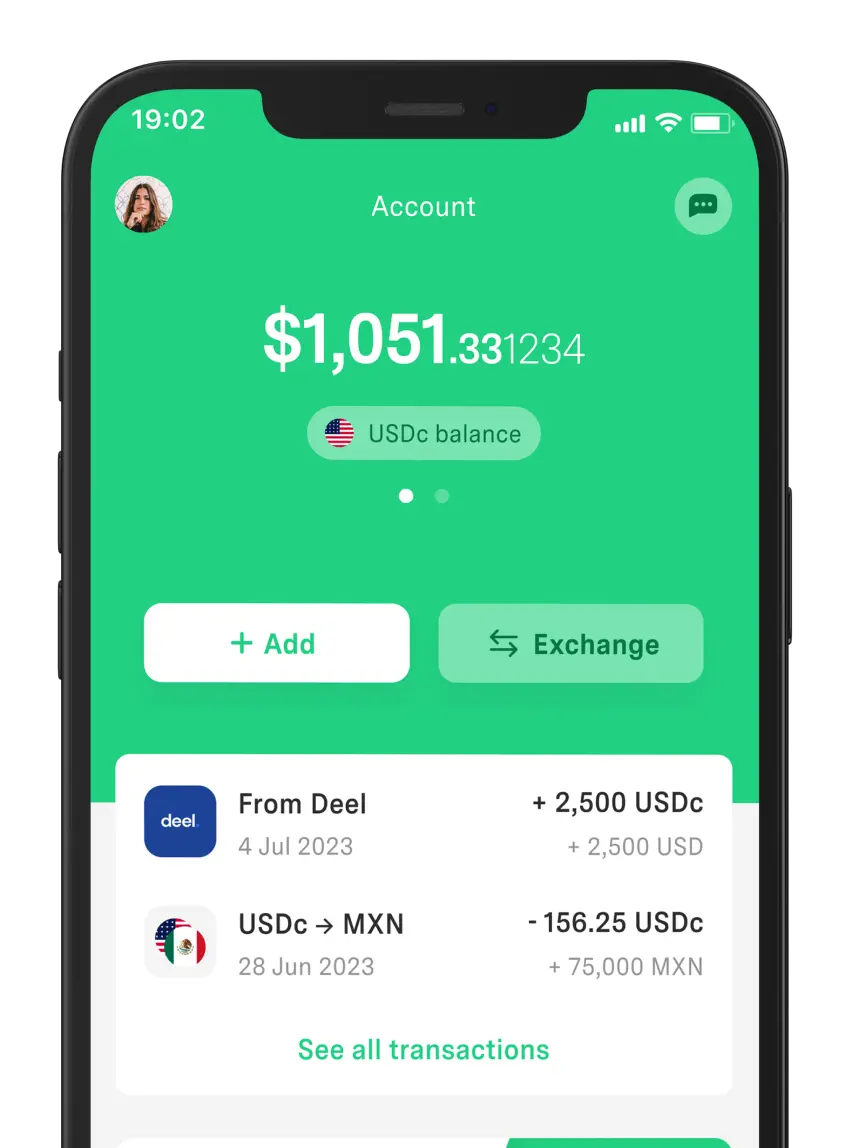

Transparency is key to blockchain—just as it is to DolarApp when it comes to managing finances. With us, you’ll find a fair exchange rate for your currency conversions and any operation in USDc or EURc.

Frequently Asked Questions

What is blockchain in one sentence?

Blockchain is a technology that records transactions in a distributed ledger organized into linked blocks and verified by a network—creating a shared, traceable history that’s hard to alter without leaving evidence.

Is blockchain the same as Bitcoin?

No. Bitcoin is a cryptocurrency that uses blockchain to record transactions and asset ownership. Blockchain, by contrast, is the underlying technology that can also be applied to logistics, identity, and records.

What is blockchain technology used for?

It’s used to record and validate information among multiple parties with a verifiable history. It’s applied in payments, product traceability, smart contracts, and identity—especially when transparency, auditability, and shared control are needed.

Is blockchain secure?

It can be very secure, but it depends on design. Cryptography and consensus make altering records difficult, though risks exist in poorly managed keys, smart contracts, networks with few validators, and low decentralization.

Which companies use blockchain?

It depends on the use case. Some companies have applied it in traceability and logistics (like Walmart), and there are digital asset platforms such as OpenSea.

Freelancer tips

Freelancer tips