Having specific and achievable financial goals is essential not only for your economic stability but also for fulfilling dreams or long-term projects. However, many people find it difficult to set financial goals for the short, medium, or long term.

Some even lose motivation when unexpected expenses arise.

Does this happen to you?

Don’t get discouraged—clear results are possible if you follow the five steps we’ve outlined for defining your financial goals. We’ll also discuss how to track them and share a few tips to help you stay on course.

Financial Goals: How to Set, Track, and Achieve Them

How to Set Financial Goals in 5 Steps

Setting financial goals helps you understand where you want your money to go and why. Just like with career goals, you need to know exactly what you want to achieve.

Each financial decision you make will become more intentional, guided by a clear purpose—helping you protect your purchasing power over time.

That’s why the first step is:

1. Define What You Want to Achieve with Your Money

Before thinking about saving, investing, or future planning, ask yourself a key question: What do you want your money to do for you?

Your financial goals should be rooted in that answer. They may include personal objectives such as:

These goals don’t have to be final—they can evolve over time. What matters most is that you start and visualize your ideal life, both now and in the future.

Is it about having new experiences, achieving security, or upgrading your lifestyle?

Once you answer that question, your goals will start to take shape.

All are valid—so long as they align with what truly matters to you.

2. Organize Your Financial Goals by Timeline

This step is key—it lets you classify each objective based on how long it will take to achieve. Doing this gives you a clearer sense of priorities and helps you choose the right financial strategies for each one.

Short-term financial goals: Up to 1 year. For example, saving for a vacation or upgrading your car.

Medium-term financial goals: 1 to 5 years. This might include pursuing a master’s degree or in an investing fund to grow your money for future projects.

Long-term financial goals: Over 5 years. These usually require more capital, such as buying a house, saving for retirement, or covering a child’s college education.

Identifying the timeline helps you figure out how much you need and how long you have to reach your goal.

3. Assign a Deadline to Each Proposed Goal

Setting a concrete date is crucial to turning intentions into actionable plans.

Let’s say one of your personal financial goals is to travel to Japan after completing your master’s degree in five years. Having that time frame helps you estimate how much you’ll need and how to spread it out over time.

Even if the date shifts later, setting a clear deadline gives structure and direction to your goal.

4. Set Priority Levels

Prioritizing helps you decide where to focus your resources first without losing sight of the bigger picture. A good way to do this is to classify your financial goals by level:

Essential: Mandatory for your financial stability, such as paying off a high-interest bank debt or building an emergency fund.

Necessary: Important for your growth but not critical—for instance, saving for a course or remodeling your kitchen floor.

Desirable: These bring satisfaction but can be postponed without consequences, like upgrading your car or planning a vacation.

This clarity works for immediate, medium-, and long-term goals alike. That way, you can move forward with structure—even if your income changes or unexpected situations arise.

5. Calculate What You Have and What You Still Need

Now it’s time to be realistic with the numbers: How much money have you already saved, and how much more do you need to meet each goal?

Let’s say you’re planning a trip to visit tourist destinations in the United States next year, and you estimate it will cost $3,000 USD.

If you already have $900 USD saved, that means you need $2,100 USD more. To figure out how much you need to save each month, divide the remaining amount by 12:

2,100 ÷ 12 = 175 USD per month to reach your goal on time.

Note: For plans like this, keep an eye on exchange rate fluctuations, as your expenses will be in foreign currency.

How to Track Your Financial Goals

The previous steps are just the beginning. To reach each of your financial goals, consistent follow-up is essential.

A good way to do this includes:

Adding Your Goals to Your Monthly Budget

Reviewing your finances regularly will show you if:

You’re progressing as expected

You need to redirect funds toward your goals

It’s time to rethink your goals due to a life change (like having a baby)

If your goal includes your family—for example, relocating—it’s important to discuss it with everyone involved. Open communication strengthens commitment and encourages teamwork.

Choosing the Right Tools for You

You can start with something simple, like a personalized spreadsheet. If you prefer more visual methods, use various types of charts, like bar charts, to track progress.

There are also apps that offer a more automated process. For example:

Fintonic: Helps you visualize your accounts and categorize expenses and income.

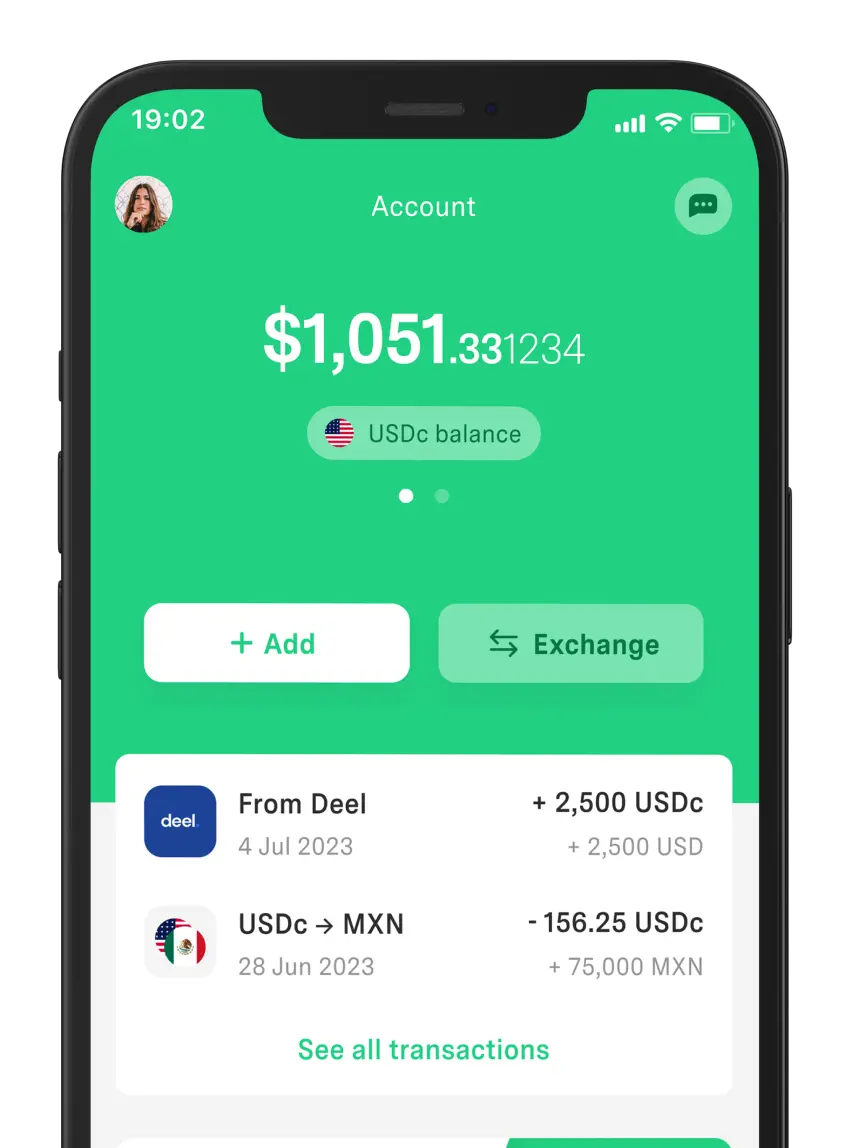

DolarApplets you open a digital dollar (USDc) account from your phone in just a few minutes. You can also convert currencies without hidden fees.

And if your goal involves shopping, traveling, or making digital payments in USD, you can request your DolarCard—an international card designed to make transactions directly in USDc.

3 Tips to Achieve Your Financial Goals

Reaching your financial goals isn't about luck—it’s about focus, consistency, and a strategy you can follow every day. These 3 tips can help you turn distant plans into real accomplishments:

1. Break your goal into smaller steps

Divide a big goal into manageable tasks so the journey feels less overwhelming. If you have short-term financial goals, like saving $12,000 in a year, focus on saving $1,000 each month.

2. Use extra income intentionally

Do you receive bonuses, holiday pay, or additional income? These can be powerful allies. Instead of spending impulsively, allocate them toward your financial goal. Taking advantage of variable income can mean several months of savings in advance.

3. Stick to the plan, even when it gets tough

It’s normal to face temptations and unexpected expenses. However, what truly makes your plan work is consistency.

Keep your mindset focused—every decision brings you one step closer to your goal.

And don’t forget to celebrate your progress. Recognizing even small wins will give you the boost you need to keep going.

FAQs: Financial Goals

How can I prioritize different financial goals?

Start by identifying which goals can’t wait, such as building an emergency fund. Then, organize the others based on importance and the time required to achieve them. This way, you can allocate your money wisely without neglecting essentials.

Why is it important to have financial goals?

Because they help you make mindful decisions about your income and spending. At the same time, they prevent you from using your money aimlessly and allow you to track your progress over time.

What are the characteristics of good financial goals?

Financial goals should be clear, achievable, measurable, and time-bound. They must also align with your personal priorities and adapt to everyday changes in your life or economic situation.

Discover a world without borders.

The world has borders. Your finances don’t have to.

Your Money

Your Money