Your Money

Your Money Is the Mexican Peso Devalued or Depreciated?

If the Mexican peso loses value, are we talking about devaluation or depreciation? Since 1994, the correct term has been depreciation. Here’s why.

Sofia Santos 9/1/2025

Remittances play a crucial role in the well-being of many Mexican families. According to BBVA Research, 96.6% of them come from Mexico’s neighboring country, the United States.

However, some people are not entirely clear on how to collect remittances in Mexico, the conditions, and the fees involved.

That’s why we’ve prepared this brief guide, where we’ll present options, steps to withdraw the money, requirements, and tips to choose the right method.

It means accessing the money that a person (family/friend) sends from abroad to Mexico. Remittances can arrive through different channels, for example, via international banking operations through SWIFT transfers or authorized agents.

In Mexico, remittances represent around 3.5% of national GDP, which gives us an idea of their weight in the economic flow. Perhaps that’s why, today, the process of collecting remittances has become increasingly flexible.

So, where can you collect remittances?

Since there are different types of remittances, you have several options, but the main ones are:

Bank deposit collection. Many banking institutions offer the service of receiving remittances through direct deposits into local accounts, although not all of them participate.

Cash collection. If you prefer to withdraw your remittance in cash, you can go to authorized branches. For example, Banco Azteca, BanCoppel, or financial institutions like Western Union.

Collection through apps and fintechs. Digital applications and e-wallets are good alternatives to receive remittances straight to your phone.

Collection at convenience stores and other establishments. Correspondents or partner supermarkets also offer the option to collect remittances.

In essence, you can choose between several viable options when receiving dollars or euros from abroad in Mexico. However, you must check what document is required, as each option works differently.

To collect remittances in Mexico, whether at a bank, branch, or through a digital app, you may be asked for certain data and documents.

In general, these are the basic requirements:

Identification of the person collecting (Mexican passport, INE, etc.), valid with a photo.

Transfer reference number or code generated at the time of sending. This code must be provided by the sender.

Basic information about the transfer, for example, country of origin, full name of the sender, and approximate amount.

Remittance form (in some cases). Some banks require completing a form with your information and that of the transfer.

These requirements allow the institution to verify your identity and validate the transfer.

How to collect remittances in Mexico?

The procedure for collecting a remittance in cash in Mexico is very similar across most banks, branches, or authorized correspondents.

Of course, details may vary from one institution to another. However, if someone sends you U.S. dollars or another currency, the basic steps are usually:

1. Go to the authorized branch or counter, whether a bank, exchange house, or correspondent.

2. Present your official ID and the transfer code the sender provided (e.g., MTCN at Western Union).

3. Fill out the form (if required).

4. Receive the cash, once the provided information has been confirmed.

Regardless of the currency used for the transfer, the payment of your remittances will be in Mexican pesos. That’s why it’s essential for the sender to carefully consider their options, especially regarding the exchange rate that may apply.

As we mentioned, when collecting a remittance in Mexico, it’s important to consider how the sent money is converted. To this, you must add any possible associated costs.

Fees. In most cases, there are no fees for collecting remittances. This is covered by the sender in the country of origin, although it depends on the company used and/or the method.

Exchange rate. The amount you receive in Mexican pesos is determined by the exchange rate applied by the provider at the time of the transaction.

Banxico usually publishes commissions, costs, and processing times of participating companies. Regarding the exchange rate, it may vary slightly compared to the interbank market.

If you receive remittances from abroad, you have several alternatives to collect them safely in Mexico:

Thanks to institutional backing, banks are reliable for withdrawing remittances.

Elektra and Banco Azteca have a network of partners that provide immediate cash delivery for remittance transfers. Among them are Western Union, MoneyGram, and Ria Money Transfer.

7-Eleven, Oxxo, pharmacies, as well as some supermarket chains, operate as authorized correspondents for remittance payments.

But when it comes to convenience, the most practical solutions are:

Bank transfers, which are secure and avoid handling cash.

Digital wallets, like PayPal, the U.S. company with the widest global reach.

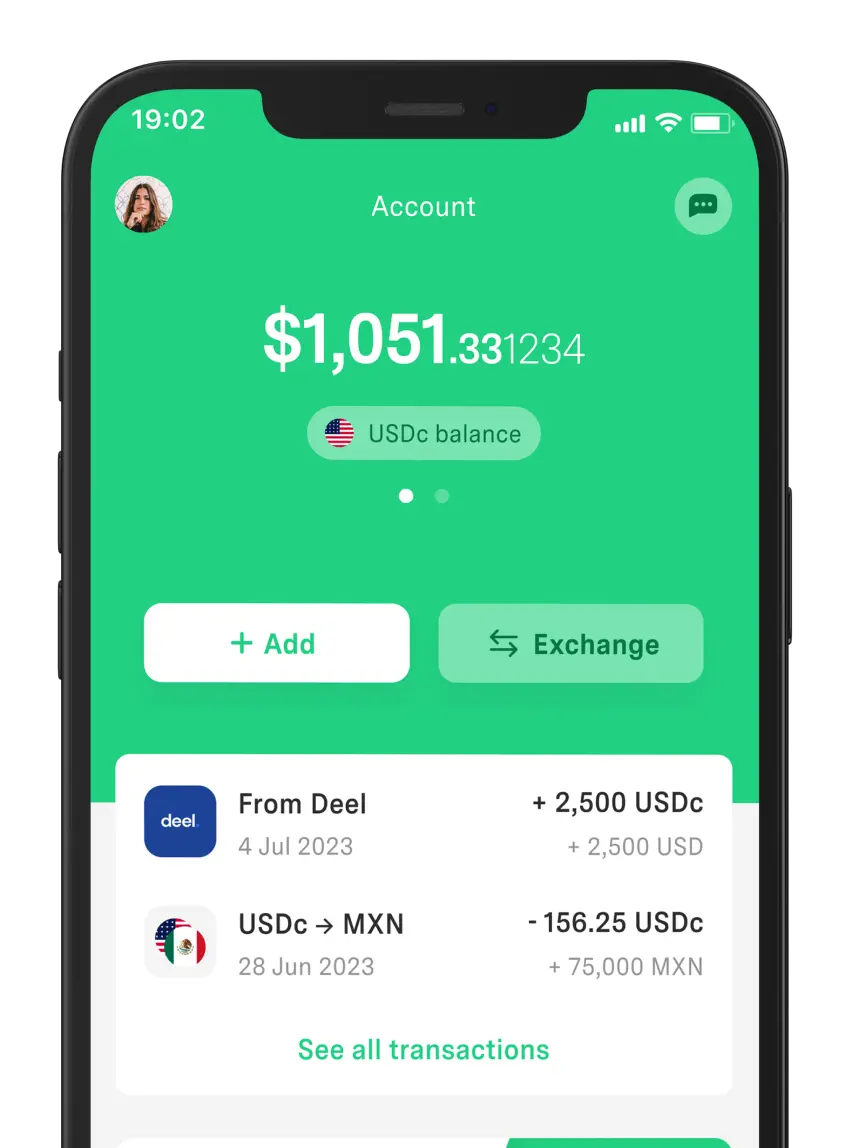

Mobile apps and fintechs, for example, DolarApp, since our app allows you to receive remittances into a digital account, quickly and with a fixed fee of 3 USDc regardless of the amount you receive.

The following table summarizes the different ways to collect remittances in Mexico:

Option | How to Collect? | Advantages |

Traditional banking | Direct deposit to CLABE in national banks. | Secure, institutional backing. |

Cash at branch | Services like MoneyGram or Banco Azteca. | Immediate and accessible. |

Apps / digital accounts | Fintech like DolarApp. | Fast, no physical cash, lower fees. |

Convenience stores | 7-Eleven, Oxxo, or other correspondents with code and ID. | Extended hours and wide coverage. |

Despite the recent decline in remittance inflows to Mexico, they remain a crucial part of the country’s economic and social context. That’s why we recommend analyzing the available options, as well as:

Compare exchange rates between banks, fintechs, and branches before collecting.

Avoid unregulated intermediaries to ensure your money arrives safely.

Verify the transfer code and that the sender’s name is spelled correctly to avoid delays.

Prioritize your personal safety if collecting remittances in cash. Try to go during safe hours and to official branches.

Stay well-informed about tax issues, as there are situations where you may need to pay taxes on remittances.

It’s also important to check if there’s a limit on how much you can withdraw. As with other aspects, this varies by provider.

There are various options for collecting remittances; you just need to evaluate which works best for you. For example, if you need the money immediately, withdraw cash at nearby stores or banks. But if you’re not in a rush or want to avoid handling cash, digital apps are a good option.

With DolarApp, you can collect remittances quickly and securely. We offer you access to a digital account in USDc and EURc without leaving Mexico.

You can do everything directly from the mobile app.

In addition, we offer a competitive exchange rate for buying and selling USDc/EURc, and you can also send digital dollars to the U.S. You’ll only be charged a flat fee of 3 USDc per transaction, regardless of the amount.

Yes, it’s possible with services like Western Union, MoneyGram, or Banco Azteca and their collection points for cash withdrawals. In general, an official ID and a reference code are enough.

Each institution sets a specific deadline to withdraw the money, usually 30 days. If you don’t collect it in time, it will most likely be returned to the sender. You would then need to resend it to be able to collect it.

Mexico does not have a single legal limit, but each provider sets caps per operation/day. However, very high amounts may require additional verification or be reported to the SAT.

Los países tienen fronteras. Tus finanzas, ya no.

Your Money If the Mexican peso loses value, are we talking about devaluation or depreciation? Since 1994, the correct term has been depreciation. Here’s why.

Your Money

Your Money Fines or debts with the SAT will only make your tax situation worse. Read this post to find out where to check and what to do if you have one.

Escanea el código y únete al movimiento global