When you travel, you shouldn’t have to worry about how much you’ll be charged for paying in another currency. Yet it happens when you use a card that works abroad but isn’t fully transparent about its fees or applies conversions at an unfavorable exchange rate.

To avoid that, we’ve put together an updated list of the 7 best cards for international travel in 2026. You’ll find no-annual-fee options, premium alternatives with perks, and solutions like DolarApp to save, stay in control, and gain clarity.

The idea is to choose the best travel card for your needs—with clear terms and conditions. That way, you compare what matters most: fees, exchange rate, and cash-withdrawal charges.

The 7 Best Cards for Traveling Without Hidden Fees in 2026

1. DolarCard: Prepaid card with no foreign transaction fees

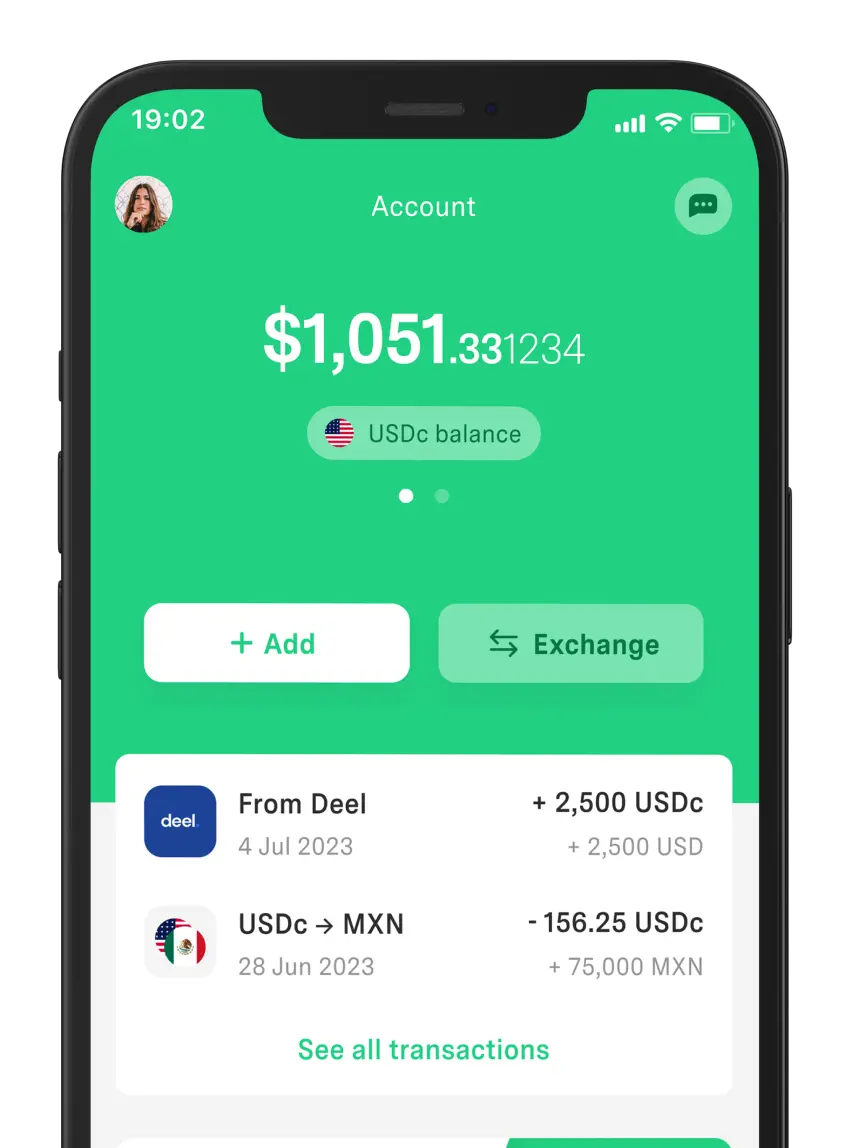

If you want transparency and control from your phone, DolarApp offers DolarCard, a prepaid card with no foreign transaction fees.

It’s a Mastercard prepaid card with domestic and international coverage. Simply put, it lets you pay anywhere in the world without surprise charges, whether in dollars or euros.

Why is it the best card for paying abroad?

Control. Fast issuance, in-app management (limits, lock, tracking), and bank-data integration to make moving money easier. No annual fees or maintenance fees.

Real-time conversion. You can instantly exchange currencies from the app, for example, from USDc (digital dollar) to pesos or vice versa, at a fair exchange rate.

Transparency. No hidden surcharges on international purchases, with clear rules for paying in another currency and visible rates in the app.

Ideal for Latin American travelers and businesses that need spend controls and cleaner payments.

Plus, with the app you can make international transfers for a flat 3 USDc/EURc.

Travel insurance. Coverage for lost or delayed baggage (up to $1,500 USD) and global assistance for medical emergencies abroad (up to $100,000 USD). Ideal for international travelers.

Scene+ rewards. Earn 5 points per $1 CAD at restaurants/food delivery & entertainment, and up to 6 points per $1 at participating grocery stores.

Purchase APR: 20.99% (variable). Best for frequent travelers who also want strong local value and flexibility.

Pro tip: As it’s American Express, check acceptance with some merchants; it generally works well for travel, but it isn’t universal.

7. Tangerine Money-Back World Mastercard: no annual fee and travel-friendly cashback

Tangerine Money-Back helps with budgeting as a no-annual-fee card. That means no yearly cost for using the credit card; it also stands out for:

Category cashback: choose 2 or 3 categories and earn 2% (if you deposit cashback into a Tangerine Savings Account); 0.5% on other purchases.

Auto-deposit of cashback into your Tangerine savings account.

Useful as a backup or contingency card for international trips.

Note: Foreign-currency purchases incur a 2.50% conversion fee on the converted amount.

If you prefer another no-annual-fee option, Wells Fargo Attune is similar but charges 3% for currency conversion/foreign transactions.

How to Choose the Best Travel Card Without Hidden Fees

The best travel card is the one that’s transparent about charges and fits your travel style. If you travel often, paying an annual fee for more perks might make sense. If you travel occasionally, a no-annual-fee option may be enough.

Compare these criteria:

Foreign transaction fee. Confirm it’s 0% or whether a percentage applies for non-local currency. Prioritize “no foreign transaction fee.”

Exchange rate. Check for a competitive conversion rate—visible in-app or on your statement.

Rules & exceptions. Look for limits, monthly caps, and fine print that could trigger unexpected charges.

Annual fee vs. benefits by travel style

Premium cards: higher upfront cost, but more advantages (lounges, insurance, credits) if you travel frequently.

No-annual-fee cards: lower maintenance, simpler protections—often enough for occasional trips.

To make it easier, build a comparison table covering: foreign transaction fees, travel insurance, rewards, acceptance, and spending requirements. Decision = much clearer.

Key Factors to Avoid Fees and Maximize Travel Benefits

On trips, surprise costs rarely come from a single big purchase. They creep in through details—like foreign-currency surcharges or rewards that don’t apply as expected.

A foreign transaction fee is a surcharge some cards add when you pay in a foreign currency—often 2%–3% of the purchase.

So check:

The terms. Look for “no foreign transaction fee.” If you don’t see it, assume there could be a surcharge.

Rewards rate. Compare how much you earn on travel (flights/hotels/transport) vs. everyday purchases.

Included insurance. Review medical coverage, baggage delay, and cancellation/interruption—limits and requirements.

For example, if your card includes trip cancellation, verify the maximum amount, when it applies, and what documentation is required.

Practical Tips for Using Cards While Traveling—And Avoiding Hidden Costs

Hidden costs usually come from currency conversions, ATM withdrawals, and fees you didn’t expect.

Carry two cards—a primary and a backup. If one fails, you won’t rely on cash or high-fee ATM withdrawals.

Consider a prepaid card with no foreign transaction fees, e.g., DolarCard from DolarApp.

With these habits, you’ll reduce surcharges and travel with more control from day one.

Additional Benefits: Travel Insurance, Lounges, and Rewards Programs

While a no-fee structure is great, the most value can come from the perks you actually use—like travel insurance.

Here’s what premium cards can cover:

Premium card

Lounges

Travel insurance coverage

Rewards/value

American Express Platinum (Mexico)

Priority Pass Prestige (lounge access per program terms).

Medical emergencies, cancellation/interruption, delays, baggage, among others.

Membership Rewards + travel benefits and premium credits/perks (per plan and terms).

Capital One Venture X

Access to 1,300+ lounges (Capital One + Priority Pass, after enrollment).

Cancellation/interruption, delays, baggage, and rental-car related coverage, among others (per terms).

10x hotels/cars & 5x flights via Capital One Travel; 2x on everything else.

Scotiabank Passport Visa Infinite (Canada)

Visa Airport Companion: 6 free visits per year + access to 1,200+ lounges (per program).

Emergencies, cancellation/interruption, flight delays, among others. Detailed coverages in kit/certificate

Bonuses/promos: up to $400 per terms.

Note: Always review the specific terms and conditions; they depend on your country, issuer, and the current program.

For travel, premium cards stand out for tangible benefits like these. But you can also get great advantages from international credit cards—wide acceptance and useful protections.

That said, a prepaid card can still be the best travel card without hidden fees. If you live in Mexico, Colombia, Argentina, or Brazil, DolarCard is one of the most convenient options. Just request it in DolarApp, load funds in USDc or EURc, and use it abroad.

Frequently Asked Questions

Which cards are most recommended with no foreign-currency fees?

The best are those that don’t add surcharges when paying in foreign currency—for example, certain digital prepaid and international cards that convert at a clear rate with no hidden fees.

What ATM-withdrawal limits do these cards offer abroad?

Some cards include a limited number of free withdrawals per month. Limits, caps, and ATM fees depend on the product, issuer, and even your plan.

How can I avoid hidden fees when paying by card abroad?

Choose a card with no foreign transaction fee, pay in the local currency, and avoid the merchant processing the conversion. Turn on alerts to spot extra charges.

What insurance and protections do travel cards offer?

They may include medical assistance, delays, baggage, and trip cancellation/interruption—depending on the card. Review conditions, caps, and requirements before traveling.

Is it advisable to carry more than one card on an international trip?

Yes. Carry two on different networks in case one fails or isn’t accepted. This helps you avoid relying on cash and reduces urgent ATM withdrawals that often carry fees.

Trabalho e viagem

Trabalho e viagem