In 2026, cross-border payments have become part of everyday life for freelancers, digital businesses, and anyone receiving money from abroad. But the reality is that the final cost and time to arrive can vary widely from one platform to another. That’s where doubts often arise: Which one is the best value? How transparent is it?

So if you’re looking for the best fintech app for borderless transactions, this article is for you.

Here you’ll find a clear comparison so you can choose the option that best fits how you operate—whether that’s charging clients, paying suppliers, or simply moving funds between countries.

Best fintech platforms for cross-border payments in 2026

What are cross-border payments?

Cross-border payments are transfers that move money from one country to another. They also involve regulation, currency conversion, and settlement methods to ensure funds arrive safely to the recipient—via banks, payment networks, or fintechs.

Criteria for choosing a cross-border fintech

Between fintechs, speed, real costs, available currencies, and your level of control over each payment can all change. In other words, they don’t all work the same way. That’s why it’s essential to evaluate certain criteria before choosing an app for sending money or making international payments.

This checklist can help you compare options quickly and objectively:

Speed. Resources can arrive instantly, within 24 hours, or in several days depending on the country, currency, and network used.

Total costs. Add the fixed fee and the FX spread (the difference between the real exchange rate and the one applied by the platform).

Currencies, assets and methods. Confirm which currencies or assets the fintech supports and how you can send, pay or receive: bank transfer, card, digital wallet, or other options.

Security and compliance. Check that it requires identity verification (KYC) and has anti-money-laundering controls (AML) to avoid blocks and fraud.

Reconciliation and reporting. Make sure you can download receipts and reports to control payments, organize inflows/outflows, and simplify accounting.

Transparency and traceability. See whether you can follow the payment status and track the transfer or follow up on the transaction until it’s credited.

Smart routing (if applicable). Some fintechs pick optimized payment routes to reduce costs and time depending on country, currency, asset and available network.

With this list, you can compare platforms in minutes and stick with the one that best fits.

Quick comparison of cross-border fintech platforms (2026)

If you’re looking for the best fintech app for borderless transactions, this table compares the main platforms:

Fintech

Average time

Total costs (fee + FX)

Currency

Supported methods

DolarApp

Instant (~10 s via SEPA) / < 24 h / 3–6 business days, depending on route

App, SEPA, SWIFT transfer, ACH, Wire, Mastercard card, Apple Pay, Google Pay

Wise

Instant (~20 s) / < 24 h (95%) / up to 2 business days, depending on route

Variable: fixed fee + percentage by route and currency (from ~0.33%) + transparent FX

40+ currencies

Bank transfer (ACH, SWIFT, Wire), card, debits (by country), Apple Pay, Google Pay

Stripe

2–3 days (may vary); first payout: 7–14 days

Variable: per-transaction fee + FX if applicable

135+ currencies

Cards; bank debits (ACH, SEPA Direct Debit); Apple Pay, Google Pay; varies by country

Payoneer

Instant / 1–3 business days, depending on route and method

Variable: service-based fees + FX (conversion up to 3.5% in some cases)

Multi-currency

Payoneer account, bank transfer, Mastercard card (by country), ACH/local transfers

Best fintech for international payments

In this section, you’ll find options competing to be the best fintech app for borderless transactions in 2026. Below is a mini-review of each:

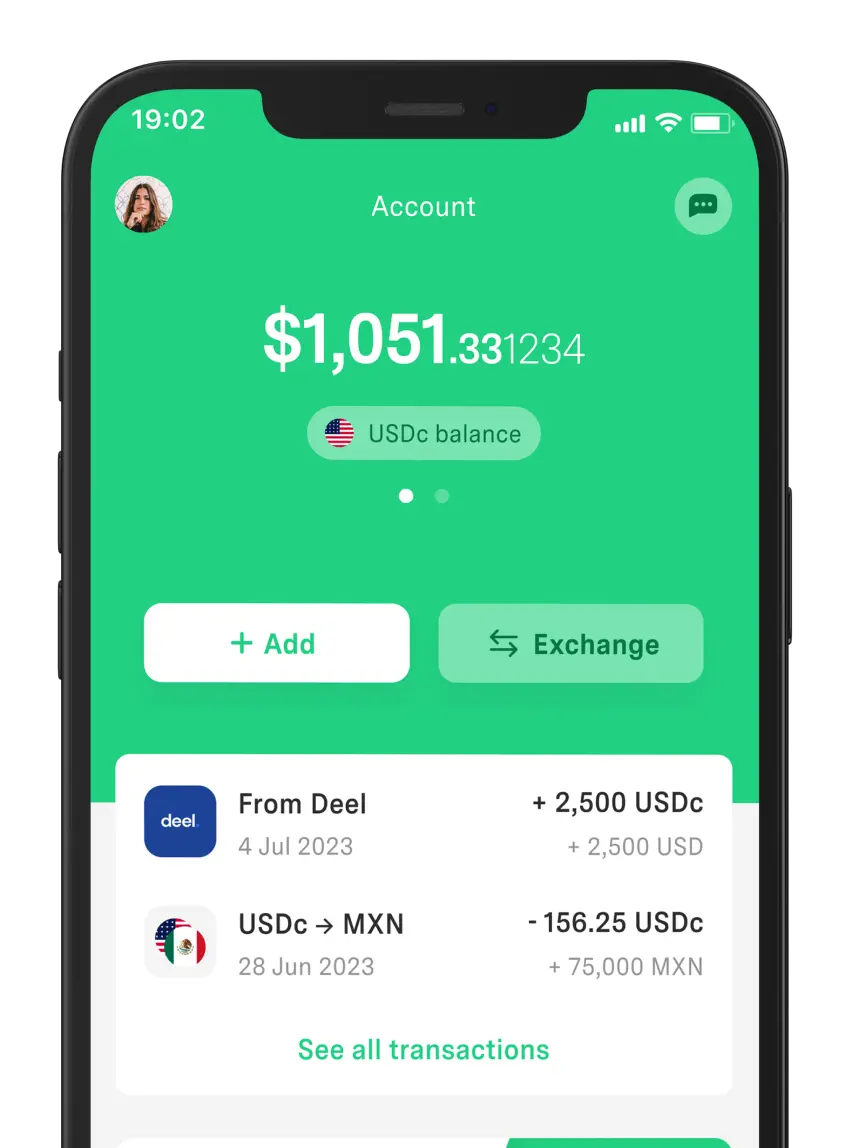

DolarApp

An app designed for Latin American users (Mexico, Colombia, Argentina, and Brazil). It lets you operate with digital USDc/EURc, move assets cross-border with simple costs, and convert between currencies from your phone.

Pros: LATAM focus, international Mastercard card, easy-to-understand fees, and transparent exchange rate or conversion rate.

Cons: Not the best choice if you need complex infrastructure.

Best for: Individuals and freelancers in LATAM who want to manage USDc/EURc from their phone, pay in different currencies, and keep control of their costs.

Ideal if… You want a simple day-to-day experience and prioritize cost clarity when moving money or paying abroad.

Pros: Wide multi-currency support and transparent cost calculation before you confirm.

Cons: Fees depend heavily on payment method and route, and some features vary by country.

Best for: Those who pay or get paid in different currencies and want a flexible solution for moving founds across countries.

Ideal if… You make frequent international payments and need a practical option for converting and transferring without surprises in total cost.

Stripe

Built for those who need to take online payments from international clients.

Pros: API-first, very complete ecosystem, multiple payment method support, and good flexibility for operating across countries and currencies—scalable for e-commerce and SaaS.

Cons: Not a personal-use app; requires technical setup, and the relevant time metric is usually payout speed to your bank.

Best for: Companies, entrepreneurs, and product teams who need to process global payments, subscriptions, or recurring billing with a robust solution.

Ideal if… You want to accept international payments on your website or app and need solid infrastructure to grow without switching platforms.

Pros: Popular for B2B and marketplaces, simplifies collecting from overseas, offers bank withdrawals, and supports multiple currencies.

Cons: Costs vary by service, country, and FX conversion. Card availability and features depend on the country.

Best for: Freelancers, suppliers, and marketplace sellers.

Ideal if… You work with platforms or international clients already using Payoneer.

Honorable mentions

Adyen, Rapyd, Airwallex, and Conduit are worth considering if you’re seeking a more enterprise solution for cross-border payments. These platforms are often alternatives for more complex or large-scale operations.

2026 trends impacting international payments

In 2026, the difference between a slow transfer and a more efficient one often comes down to the technology and rules each platform follows. These are the trends shaping cross-border payments:

All-in-one fintech. More platforms integrate payments, FX, cash control, and compliance to simplify processes and provide better cost visibility.

Stablecoins and CBDCs. Stablecoins continue gaining ground as a faster way to move value, while CBDCs progress through pilots and new rules in different countries.

Alternative methods and interoperability. Local methods and connections between systems are growing so international transfers can flow more smoothly among banks, wallets, and fintechs.

Automated compliance. Platforms are adding automated rules for checks, limits, and controls to reduce friction without sacrificing security.

In short, international payments are becoming faster, more integrated, and more controllable.

Tips for choosing the best cross-border fintech platform in LATAM

If you’re in Mexico or elsewhere in Latin America, you’ll agree that finding fast, low-cost international payments doesn’t depend only on the fee, right? The method you use, the exchange rate, and operational quality also matter. That’s why we recommend:

Choose a secure platform that works well in your country.

Prioritize options where you can see the fee and exchange rate at a glance.

Make sure it supports the currencies you actually need.

Review limits, fees, and conditions before sending large amounts.

Compare benefits between platforms (e.g., Revolut and DolarApp) to choose what best fits your operations.

Before deciding, simulate the same amount across two or three platforms to see how much arrives net and how long it takes.

If you run a business, evaluate whether opening a U.S. LLC would help you collect payments, organize finances, and access more international payment options.

Conclusion

In 2026, the most important thing when choosing a fintech for cross-border payments is getting clarity, control, and real value. The difference usually lies in fees and FX, speed, your country, and the currencies you need.

That’s why it’s worth opting for solutions that make the process simple and transparent from the start. And DolarApp is a practical alternative for keeping control of your costs on every move.

Besides sending and receiving USDc/EURc, we offer a fair, visible rate to buy or sell currencies—everything in a few steps from the app.

Frequently asked questions

Where can I find the best global payment service in fintech?

On platforms that display total cost and have clear methods and fees (like DolarApp). It should also be secure, work well in your country, and fit your personal or business needs.

Which fintech company offers the best borderless transactions?

It depends on your country and the type of operation. For movements between Mexico and the U.S., options like DolarApp and Wise often stand out; in some markets, Revolut as well.

What’s the best fintech for borderless transactions?

In Latin America, DolarApp often works very well to manage digital USDc/EURc from your phone. But if you need to handle many other currencies, Wise may be a more complete option.

Which company is faster and cheaper?

It varies by method, currency, and country. However, DolarApp is often one of the more competitive alternatives in LATAM thanks to its simple cost structure—Wise as well.

What factors affect the total cost of an international transaction?

The fee, the applied exchange rate, and the method used. Even local payment options or newer alternatives can change cost and speed by country.

Your Money

Your Money